July 20, 2018

July 2018 Outlook

In FY 16-17, fuel prices were 124c per litre on a national average, whilst diesel’s average at the same time was 125c per litre. In FY 15-16, they were 122c and 123c average respectively.

We roll the clock forward to the current period and fuel is closer to 150c per litre and diesel up to 155c per litre. By the lowest measure, the price increase has been + 16% & 17% respectively. Four regional banks have very recently increased domestic mortgage borrowing rates and it appears highly likely that the major’s are not too far behind them, again.

Australian residential building approvals released 3rd July were slightly weaker than market expectations in May, falling 3%, after a 5% decline in the previous month. According to ANZ Research, this supports their view that the peak of housing finance has passed. Coupled with that view that also support, we anticipate even further tightening of credit availability across the spectrum. This is already in place for wholesale borrowers and the Royal Commission’s findings will only add to this.

Sydney auction clearance rates are closer to 50% with Melbourne’s clearance rates also abating. Our note of caution though when using this measure to assess the ‘temperature’ of residential real estate, is that other forms of sales are called upon so a better measure is the number of dwellings which have cleared. Not necessarily all at auction.

It is our opinion, that as funding becomes more expensive and more difficult to obtain, business conditions will tighten and ultimately be a drag on growth. Notwithstanding, the fintech sector stepping in to replace some of the core bank business, which will have a higher cost imposition anyway.

It could be argued that a rate tightening has occurred/been occurring and by the time it is realised and the domestic economy has awoken, it will be seen as a past event.

The reality is that the RBA cash rate has little or no impact and reference to the cost of borrowing of funds today. If the continual jaw boning by the RBA governor is then validated by a move upwards in the overnight cash rate, most if not all of this movement will already have been passed on to borrowers. If there is any doubt around this, a review on historical cost of funds should clarify any ambiguity.

Inflation remains stubbornly low while fixed rates have eased based upon geo political influences around trade for a large part. US treasuries have also eased around this uncertainty and the crystal ball gazing into future predictions at this time is very clouded in our view. On other occasions, it appears less so.

[1]Australian Institute of Petroleum

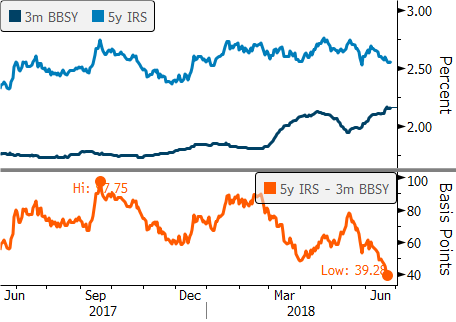

BBSW Funding

In our last Outlook, we provided a synopsis around the rise in BBSW and RBA Repo funding. Whilst we do not intend to go over this again, we are always prepared to stand by our views and adjust our opinions as necessary due to anecdotal and/or overwhelming data. An excerpt of the previous paper was:

“Expectation by some forecasts is that as 3m BBSW as gets closer to 2%, with the RBA on hold indefinitely, that demand for yield will be sufficient to cap and reverse the spread, although the US linkage will likely keep the spreads wider than previously.”

What did transpire was that 3m BBSW has been consistently above 2.00% 1m BBSW has been setting at above 2.00% over the past week. The complexities around why this occurs we believe is similar to our prior analysis. However, this funding pressure of variable rates directly impacts any borrower on a floating rate basis, but there is also another angle that manifests, which is that fixed term rates have eased from their highs. Simply put, the cost of carry, being the spread between fixed and floating rates has narrowed significantly. This creates attractive hedging opportunities.

So, there has been another push higher in BBSW over the past month as funding pressures emerged into end of quarter. BBSW is now setting at 2yr highs even though the market is pushing out RBA hike expectations. The market doesn’t have a rate increase priced until 2020

Previously,

“The cost of carry; as quarterly BBSW has pushed out, one of the resistance points of the corporate borrower has been the reluctance to pick up the cost of carry, ie, the difference between the fixed rate of a swap and the floating index being either BBSW or BBSY. This has now narrowed to around 30-40 bpts. This can be considered balance sheet insurance.”

Currently,

The cost of carry of a 3 year quarterly fixed rate vs BBSW is now 4 bpts. The cost of carry over a 5 year hedge on a quarterly basis is around 22 bpts. Whether the benchmark is BBSW or BBSY will produce the same spread.

Table 1² – Spread between long and short term rates.

Moves in short and long term rate markets has caused the spread between BBSY and 5yr IRS to halve over the last month.

Long term rates are currently near the lowest level see this year due to the potential hit to global growth from an all out trade war between the US and China. This is being further clouded by other economies being impacted.

Whilst the fall in term rates could be at odds with the continued recovery seen in the US economy. US unemployment is now at a 18yr low, which was a factor in the Fed’s June rate hike decision and forward guidance of 3-4 more hikes to come in the next 12 months.

As a result, the difference between long and short term rates is at its lowest level for the year. This creates an opportunity for all borrowers to take balance sheet insurance.

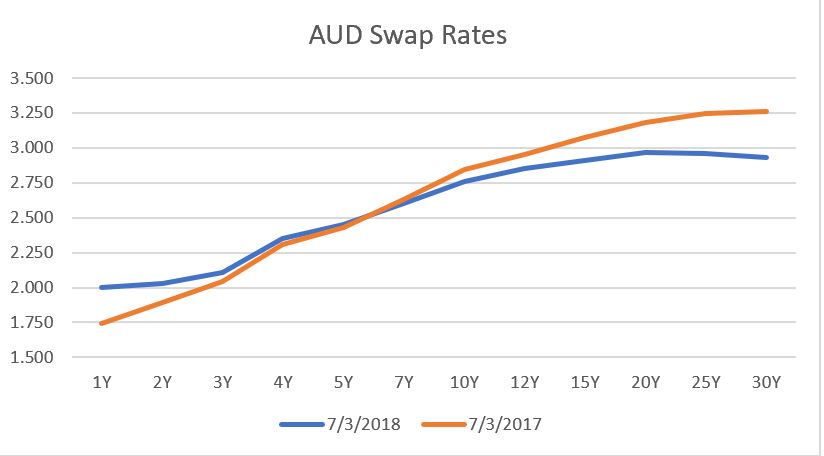

For reference, we have provided a yield curve comparison chart from 2017 and 2018.

Please note that above rates are all as per market convention, so the longer term rates are based on semi annual payments.

We welcome you to contact us with our colleagues at Stamford Capital around any strategy, risk management and funding requirements you may have. We have recently been able to find to solutions for offshore purchasers and stock overhang.

Russell Maisner

Director, Global Treasury Risk Management Pty Ltd

Email: Russell@ecommplanet.com

Ph + 61 (0)401 125858

¹Australian Institute of Petroleum

²ANZ Research